This is an election year, so there was a lot of finger-pointing. Currently, the U.S. is experiencing inflation, so it was a talking point. In this series of articles, we’ll answer some questions about inflation: what is it? How does it happen? And how can it be fixed? Then, you can decide who’s responsible or whose approach to fix it you think makes the most sense.

What is inflation?

The definition of inflation may not be as straightforward as you might think. Most people will agree that inflation is the increase in prices of things consumers buy and a decrease in consumer purchasing power.

The Consumer Price Index

The US Bureau of Labor Statistics tracks the Consumer Price Index (CPI) monthly. The CPI is measured using the average cost for a basket of goods and services for food, utilities, fuel, services, and major purchases.

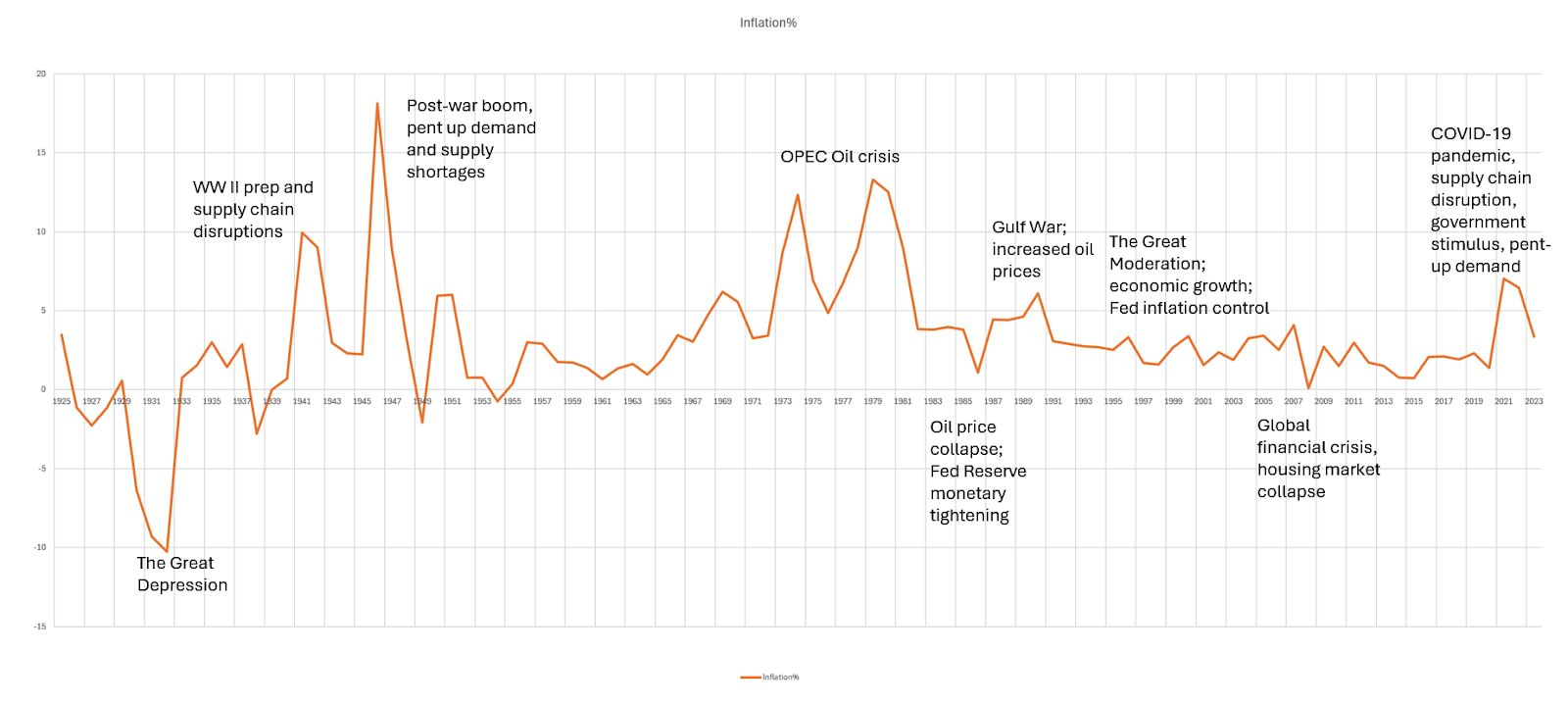

Inflation % 1924 – 2023

Percent increases in the CPI measured monthly year-over-year are the most common measure of inflation. Any increase in the CPI is inflation, but most sources consider a 2-3% increase sustainable. So, a certain amount of inflation is not intrinsically bad. The experts think that because your money will inevitably be worth less next year, there is some incentive to spend it now. Current spending drives a healthy economy.

The thinking of consumers who are not economists tends to be, “Hey, I’m paying more for stuff I need.” Inflation is, in a very real sense, a government tax. Like a tax, it’s inescapable. It reduces purchasing power. And it’s an indirect tax on savings. If you earn 3% on your savings and inflation is 5%, you lose 2% to the inflation tax.

The negative effects of inflation include the opportunity costs of holding onto money because of the uncertainty of future inflation. Buy low, sell high, and all. Buy low, meaning spend when the cost is less. Sell high or hold when the cost is high. So, while current spending drives a healthy economy, inflation may encourage consumers to hoard goods they fear might become expensive or unavailable. We’ve seen it happen.

Because the CPI is 1) measured for a specific set of goods and services and 2) averaged over geography and time, it won’t represent everyone’s experience equally. CPI samples include households in urban areas, where those households shop, specific items, and housing in urban areas. So, if you do not represent the average household purchasing these specific items in the city, your mileage may vary. It may be worse; it may be better.

Your individual inflation rate may feel different based on how frequently you purchase goods that have gone up in price and whether your personal income is keeping up with inflation. For example, cars or TVs may be the major factor driving an increase in inflation, but you only purchase one every 3 to 5 years. All other factors being equal, you won’t be affected by those price changes today. However, rising commodity prices are often a leading indicator of inflation. Higher prices in oil, metals, and agriculture can drive up prices in transportation, business, manufacturing, and the cost of doing business, which, in turn, affect the input costs of a wide range of products.

Other inflation indicators

While the CPI may be the most commonly cited indicator of inflation, there are others.

The Producer Price Index (PPI) reflects the trend of prices that producers receive. It is an indicator of inflation at the wholesale level. Increases in prices here are due to rising import costs or supply chain disruptions. These changes will be passed on to businesses as input costs and, ultimately, the consumer. PPI is a key indicator that investors and traders often use to get a feel for the pulse of the economy. The PPI is one of the oldest continuously published metrics published by the Bureau of Labor and Statistics.

The Employment Cost Index (ECI) is an indicator of wage inflation. It measures businesses paying higher labor expenses, including salaries, wages, taxes, health care, insurance, vacation time, and other benefits. These costs are passed on to the consumer and are reflected in higher prices of goods.

Bond yields are usually a reaction to inflation. Yes, bond markets do incorporate expectations about the future, but if long-term bond yields rise, the market is already reacting to inflation and expects higher prices in the future.

Trailing and leading indicators

All of these indicators – CPI, PPI, ECI, bond yields – are trailing indicators. As a trailing indicator, inflation already exists. It’s easy to look at historical data and say, “Yep, there was inflation; the CPI increased by 3.6%.” These indicators show price changes that have already occurred.

In contrast, forward-looking indicators can help predict early warning signs of inflation. Futures markets move based on what the market foresees as the supply and demand picture. For example, agricultural futures can signal the impact of inflationary expectations of bad weather or supply chain disruptions. Similarly, Commodity Futures, Food Futures, Interest Rate Futures and Energy Futures can provide insight into market expectations of future supply and demand.

Next

Next in the series, we’ll look at – even though inflation is inevitable – how it happens. Even though the definition of inflation is fairly well agreed upon, its causes (and solutions) are not.